All about Quantitative Investing

- 9 min read

While managing your money, you often deploy a combination of research, gut, gambling, trust and of course, expertise of others. The result is often mixed – sometimes fantastic and sometimes downright miserable. What if all this was replaced by a 24 x 7 robot that watches global markets, market volatility and policy trends for you to do your job? That’s essentially what basic Quant Investing can do for you!

And at Quantifi, PL’s digital asset management wing, PL Quants use an even more improved version to maximise your returns!

In India, PL is among the pioneers of quant investing. PL’s in-house team has developed industry-first, quant-based strategies like AQUA and MADP. All details of these strategies can be found here.

Basics: Types of Investment Strategies

There are usually three approaches commonly used to manage stock portfolios- Fundamental, Technical and Quant based (Quantitative) by individuals and institutions alike.

Fundamentals based investing essentially is traditional investing, with in-depth analysis of a company’s business, management team and market opportunity to determine a stock’s attractiveness. It relies on the analyst’s ability to spot the opportunity that others may have missed to generate investing “alpha”.

Technical analysis, another traditional method, is the other extreme where one is essentially either betting with the herds or against them and hoping that one is right 6 out of 10 times. One may deploy algos to do this or one may do it with one’s own armory of tools but essentially its price volume analysis in its nature.

The third manner is one that’s called Quant Analysis based investing or “systematic” or “scientific” investing., this approach uses data-driven analysis to evaluate a broad universe of stocks. This investing style identifies historical patterns and decides to invest in specific instruments or asset classes that seem to be undervalued and exit ones that seem overvalued by constant rebalancing. And the data could be overlapping – fundamental, technical, sentiment based or macro and micro economic – all of it or some of it- on which decisions are made.

All these approaches essentially aim to get clients to the same financial destination—to help reach your goals. It may not therefore be a replacement for any style you have but a complementary fit to your portfolio.

As technology and data analytics continue to evolve, the role of quant in shaping the future of investment strategies will grow exponentially. If you’re ready to harness the power of data and strategy, then quant investing could be your ticket to a more profitable and confident investment journey.

To delve deeper into the world of quant investing and unlock its potential for your financial growth, explore our portfolio management offerings here or write to pms@plindia.com.

A Word on Quant Modelling

Quant modelling is an art by itself though the results are scientific! Both traditional and quantitative managers believe that stocks can be and often are mispriced. This means the current price of a stock is out of line with the managers’ estimate of its value, either now or in the future.

Such mispricing can come from legitimate differences of opinion about a company’s business prospects. Or it can result from any number of irrational reasons—fear and greed being the most common.

This mispricing can be detected by machines – and the attempt is to get in before others do so it can make money for you (generate alpha) more than other styles of investing. The machines often process massive amounts of data – often using the most amazing like using images (like movement of thunderstorms) or heatmaps (like mobility in business districts) to simpler stuff (like MACD or RSI on the instruments or asset class).

Image 1: Illustration of a Map tracking Global Success of Value Versus Momentum

![]()

This decision-making could happen in microseconds (High Frequency Quants) or in years (Macro Quants). These quant models could also be deep learning models (where machines learn from errors and correct themselves) or simple machine learning (back tested in discrete, linear steps) or basic models.

In recent years, a lot of these quant funds have moved away from individual security selection into ETFs to minimise the risk of not being able to exit rapidly and minimise the risk of individual stock selection due to the nature of global economics.

Making Money with Asset Class Models on ETFs!

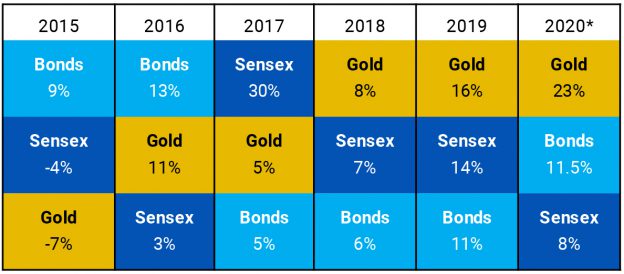

A study by Nobel prize winner Gary Brinson (along with Hood and Beebower) in 1986 of 91 large US pension funds indicated investment policy* (asset allocation) dominates investment strategy (market timing and individual security selection), such that investment policy contributes to an average 93.6 percent of the variation in the total plan return! A similar exercise conducted by Brinson in 1991 yielded a result of around 92 percent. This essentially means that if you get your asset call right, you would be ahead of most people who tried to time individual stocks within the asset class. And what better way to do this than ETFs.

Earlier however, the issue was – how do you participate in let’s say Nasdaq- through an Indian ETF or in GSecs. That’s not an issue anymore.

And hence the challenge now – how do you leverage ETFs to generate excess return and what models do you deploy to create much superior returns for clients. Too many instruments have also crowded our minds – a human mind cannot objectively process information – too much data evolving every microsecond across asset classes- and then act accordingly – how do you take emotion out! And then execute the trade in a way that doesn’t impact your profitability!

Image 2: Asset Class Returns Fluctuate- But Yours don’t need to!

This is where ETF Based Quant Models come in. Their objective – participate intelligently across asset classes based on evolving trends, avoiding individual security selection risk, and do so with adequate diversification so all prices moving down together kind of risks are minimised!

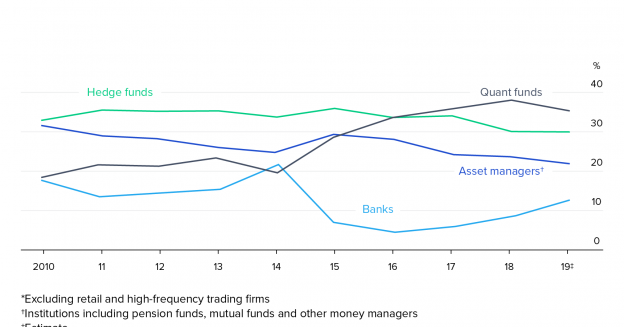

No wonder then that quant funds in the US now own more than 35.1% of market capitalisation, compared to 24.3% of human-managed funds in the USD 31 Trillion market (2019).

Image 3: Market Volume by Type of Institution in US Markets

Quant Investing in India

While there are a variety of AIFs and private pools investing via quantitative or algorithmic models, for long term investors the main opportunity is via quant-based asset allocation funds which attempt to dynamically invest across asset classes. And they have had reasonable success.

However, there are inherent disadvantages to such funds in some cases:

Most so-called quant funds use very static measures (Example, Exit Equities when PE cross 20x Historical or P/B> 2X etc) instead of recognising macro dynamics, resulting in lower exposure to momentum when it matters most. Imagine exiting markets when they first crossed 13,000 Nifty!

Many asset allocation funds use individual scrip selection, domestic or international, which results in higher expense ratios and potential liquidity issues. Remember that even 2% per annum shaved off over 10 years can mean an almost 50% difference in returns!

Many quant funds just provide guidance to the fund manager who eventually takes the call – and not the model itself – which essentially means the fund manager’s risk remains – it’s a model he is listening to at times instead of human experience, that’s all.

Finally, mutual funds are designed to be structured in a way where their asset allocations cannot breach certain levels which by nature counter acts against the model (Imagine if the model says exit asset class and the regulations don’t allow it!)

Introducing Quantifi

PL’s team of Quantamental analysts (Fundamental Plus Technical Plus Statistical) have created a product that, in its back-tests over the past decade or so, generated far superior returns than most asset allocation funds and more importantly, at far lower volatility!

An average CAGR return of 25% plus has been sustained over many years and a positive return was delivered even in 2008 when virtually all individual asset classes were decimated. And as recently as 2020, the model provided an exit out of equities, due to the nature of economic signals, even before the Covid crisis hit and then reentered equities around the Nifty 9k mark.

The above is all achieved via ETFs which in turn means low risk of liquidity, no individual stock selection risk, and low expenses as well.

We have launched two differentiated PMS strategies – which blend 80 years of our research expertise with cutting edge quantitative technology. First is the Multi Asset Dynamic Portfolio (MADP) and second is AQUA (Adaptive. Quantitative. Unbiased. Alpha-Focused). Both strategies have consistently delivered benchmark-beating returns and delivered sustainable, granular outperformance for its investors.

If the generation of regular consistent return, with low costs and low volatility, and with investments across domestic equities, international equities, govt debt, corporate debt, call money and gold, interests you, do write to us at pms@plindia.com. Alternatively, you may place the request with your relationship managers who will in turn block a session for you with our team.

Sandip Raichura

Executive Director, CEO Retail and Distribution

Disclaimer: This blog has been written exclusively for educational purposes. The securities mentioned are only examples and not recommendations. It is based on several secondary sources on the internet and is subject to changes. Please consult an expert before making related decisions.